A credit score is often seen as a reflection of your financial behaviour. Whether you plan to apply for a loan, use a credit card, or explore other financial services, lenders usually look at your credit history to understand how you manage money.

Many people believe that improving a credit score requires complicated strategies. In reality, it usually begins with simple financial habits that are maintained consistently over time.

For individuals in their working years or managing family responsibilities, building a stronger credit profile can support long-term financial confidence.

Let’s explore some practical and responsible ways to improve your credit score gradually.

Understand Your Current Credit Situation

Before trying to improve your credit score, it helps to understand where you currently stand. Reviewing your credit report can provide insight into your financial history.

Your credit report may show details such as:

Existing loans

Credit card usage

Past repayment behaviour

Active credit accounts

Understanding this information helps you identify areas where improvement may be possible.

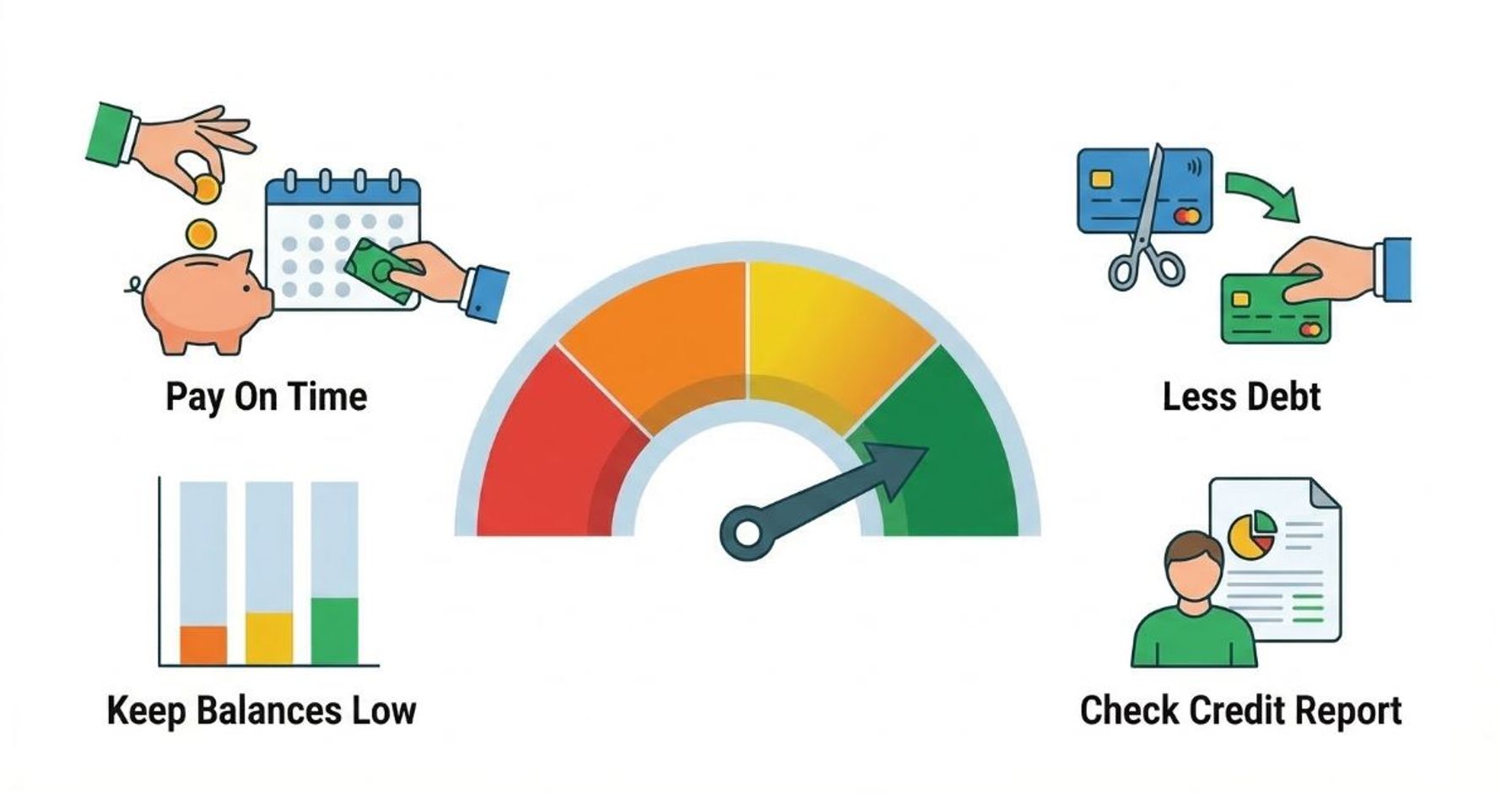

Pay Your Dues Consistently

One of the most widely recognised habits associated with healthy credit behaviour is paying financial commitments on time.

This includes:

Loan EMIs

Credit card bills

Other repayment obligations

Even small delays can affect how your financial behaviour appears in credit records. Setting reminders or maintaining organised payment schedules can support consistency.

Avoid Overusing Available Credit

Credit cards provide flexibility, but using a large portion of available credit regularly may create financial pressure.

Maintaining balanced usage often reflects better financial discipline. Responsible spending habits can gradually support a healthier credit profile.

Keep Track of Your Financial Commitments

Many individuals manage multiple financial responsibilities at the same time. These may include home loans, personal loans, vehicle loans, or credit cards.

Tracking these commitments carefully helps reduce the chances of missed payments or confusion regarding due dates.

Simple habits like reviewing bank statements and setting reminders can make financial management easier.

Avoid Frequent Loan Applications

Applying for several loans within a short period may sometimes create the impression that a borrower is under financial pressure.

Instead of making repeated applications, consider evaluating your needs carefully before seeking additional credit.

Thoughtful borrowing decisions often reflect responsible financial planning.

Maintain Older Credit Accounts Responsibly

Long-standing credit accounts that are managed well may reflect stable financial behaviour. Maintaining such accounts responsibly can contribute to a stronger credit history.

Abruptly closing older accounts without reason may shorten your credit history.

Review Your Credit Report Occasionally

Checking your credit report occasionally helps you stay aware of your financial records. This can help you notice unexpected entries, outdated information, or unfamiliar accounts.

Addressing such issues calmly and early may prevent complications later.

Avoid Ignoring Financial Stress

Financial challenges can arise for many reasons, such as job changes, business fluctuations, or personal emergencies. Ignoring repayment issues may increase stress over time. Borrowers who are managing financial responsibilities during mid-life often benefit from understanding practical debt management strategies.

If loan pressure becomes overwhelming or recovery communication causes anxiety, some borrowers explore structured guidance through platforms like loansettlement.net to better understand their options.

Focus on Long-Term Financial Discipline

Improving a credit score is usually a gradual process. It rarely happens instantly.

Consistent habits such as responsible borrowing, careful spending, and timely repayments often contribute to a healthier financial profile over time.

Financial discipline built slowly often leads to more sustainable results.

Common Mistakes to Avoid

While working toward a better credit score, it is helpful to avoid certain habits:

Ignoring repayment reminders

Applying for multiple loans impulsively

Using credit without planning

Sharing financial information under pressure

Avoiding communication with lenders when difficulties arise

Being aware of these risks can help protect your financial stability.

Conclusion

Improving your credit score does not require complicated strategies. In most cases, it begins with simple and consistent financial habits.

Paying dues on time, managing credit responsibly, and staying aware of your financial commitments can gradually strengthen your credit profile.

Financial stability is built over time, and small improvements maintained consistently often make a meaningful difference.