One of the most common questions people ask after settling a loan or credit card is: “Can I get a loan after settlement?”

It’s a natural concern. After going through financial stress, negotiation, and resolution, many individuals want to rebuild stability and restore borrowing confidence. However, loan eligibility after settlement depends on several factors, and expectations should remain realistic.

This blog explains what generally happens after settlement and how borrowers can move forward responsibly.

What Does “Settlement” Mean in Financial Terms?

Loan settlement typically refers to resolving outstanding dues through negotiation when repayment becomes difficult. It is usually considered when financial hardship prevents full repayment as originally agreed.

Settlement may bring relief from ongoing stress, but it can also leave a record in your credit history. This is why many people wonder how it affects future borrowing.

Does Settlement Affect Future Loan Eligibility?

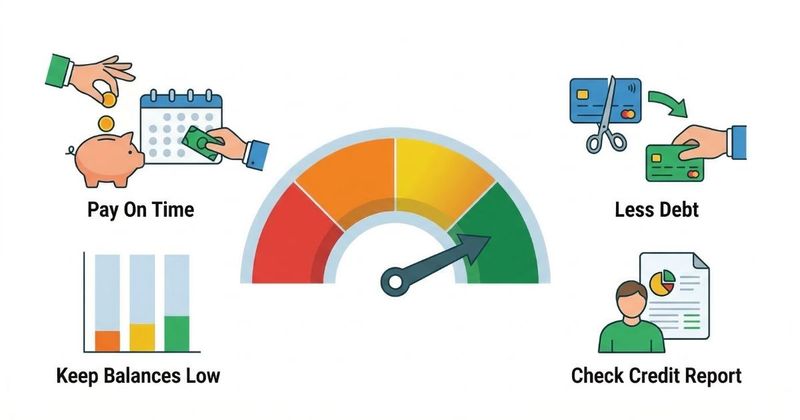

In many cases, settlement is recorded in credit reports. Lenders often review past repayment behaviour before approving new loans. Understanding how to protect your credit score after resolving debt can make a difference during future applications.

Broader discussions around debt pressure and borrower challenges in India also highlight how financial setbacks can influence future borrowing decisions.

Because of this:

- Some lenders may assess applications cautiously

- Loan terms may differ from standard offers

- Eligibility may depend on current financial stability

There is no fixed outcome for everyone. Each lender has its own internal evaluation process.

Factors That May Influence Loan Approval After Settlement

While there are no guarantees, the following aspects usually matter:

1. Time Passed Since Settlement

Lenders may look at how recent the settlement was and how your financial behaviour has been since then.

2. Current Income Stability

Stable income and clear repayment ability can improve overall financial confidence.

3. Credit Behaviour After Settlement

Consistent financial discipline post-settlement often supports rebuilding trust.

4. Existing Liabilities

Lower financial burden may reflect better repayment capacity.

Can You Rebuild Credit After Settlement?

Yes, rebuilding credit is often possible over time through responsible financial habits. This may include:

- Paying all dues on time

- Avoiding unnecessary borrowing

- Keeping financial commitments realistic

Credit rebuilding is gradual. It requires patience and discipline rather than quick fixes.

Common Misconceptions About Loan After Settlement

Many borrowers also believe common assumptions about debt handling that are not always accurate. Learning about loan resolution myths and misconceptions can help avoid confusion.

Myth: Settlement Means You Can Never Get a Loan Again

This is not necessarily true. Settlement may affect evaluation, but it does not automatically block future borrowing.

Myth: A New Loan Will Be Approved Quickly After Settlement

Approval depends on lender policies and individual circumstances.

Myth: You Should Immediately Apply for Multiple Loans

Frequent loan applications can create additional complications. Careful timing is important.

Should You Apply for a Loan Immediately After Settlement?

Applying immediately may not always be advisable. Many individuals focus first on:

- Stabilising finances

- Improving credit behaviour

- Strengthening income clarity

Rushing into borrowing again may create additional pressure.

Role of Financial Awareness After Settlement

After settlement, the priority should be long-term stability rather than immediate borrowing.

Financial awareness can help individuals:

- Understand credit reports

- Improve repayment habits

- Avoid repeating past mistakes

- Build confidence gradually

Some individuals seek guidance for clarity during this rebuilding phase.

Is a Loan After Settlement Always a Good Idea?

Before applying for a new loan, consider:

- Is the loan essential?

- Will repayment feel comfortable?

- Does it align with long-term goals?

Borrowing should serve a purpose, not add new stress.

Conclusion

Getting a loan after settlement is not a simple yes-or-no situation. It depends on multiple factors such as credit behaviour, income stability, and lender policies. While settlement may influence evaluation, it does not permanently define your financial future.

With responsible financial habits and realistic expectations, many individuals gradually rebuild confidence and stability over time. The key is to focus on long-term discipline rather than quick approvals.