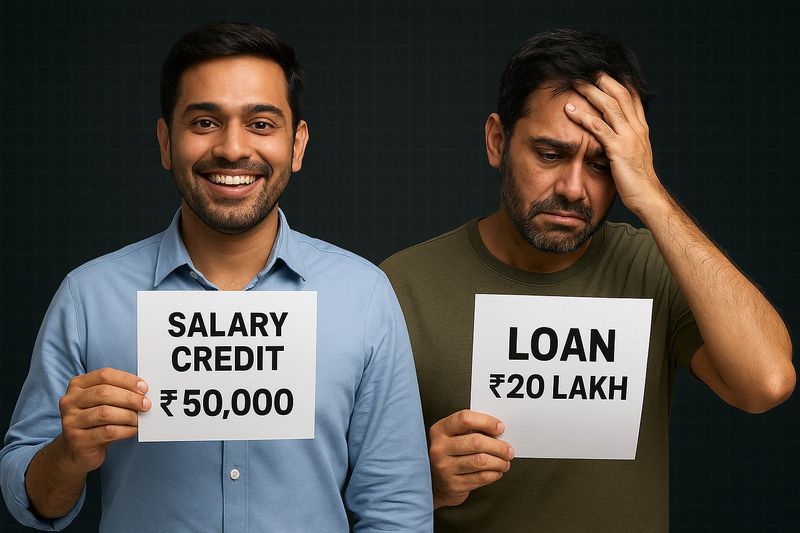

“Socha tha ₹80,000 ka phone lene se life upgrade ho jayegi… par reality? 24 mahine ka mental torture shuru!” The EMI culture has made instant gratification easy — but at a heavy long-term cost. Whether it’s a phone, laptop, or bike, small monthly EMIs create an illusion of affordability, while silently draining your future income. In this article, we’ll uncover how EMI traps work, what hidden costs you ignore, and how to protect yourself legally if you ever fall behind on payments.

The Hidden Truth About “Easy” EMIs

An EMI of ₹5,000 per month sounds harmless, right? But when you factor in interest rates, late fees, processing costs, and hidden charges, that ₹80,000 phone can easily end up costing ₹1.1 lakh or more! The real trick banks and NBFCs play is psychological — they sell affordability, not accountability. Even a short default can lead to harassment. Recovery agents are now active everywhere — calls, WhatsApp, doorstep visits — and many don’t hesitate to use intimidation tactics. If this sounds familiar, you’re not alone. Thousands of borrowers face similar experiences every month.

Why EMI Culture is Dangerous

When you take multiple EMIs, you’re not just paying for products — you’re mortgaging your future earnings. Smart financial planning means knowing your limits and rights. Here’s what financially aware individuals do: ✔ Spend no more than 30% of their income on EMIs. ✔ Read the entire loan agreement, including fine print and hidden charges. ✔ Keep digital proof of every payment for legal backup. ✔ Check the Effective Annual Rate (EAR) — not just the monthly EMI. ✔ If default seems possible, request loan restructuring (a legal right, not a favour). �� You can read more about your legal rights as a borrower on RBI’s official site.

Legal Remedies Against Loan Harassment

If recovery agents cross their limits or use threats, you have protection under Indian law:

RBI Guidelines on Fair Practices Code for Lenders: Agents cannot use abusive language or visit your residence at odd hours.

Section 506 of the IPC (Criminal Intimidation): You can file a complaint if threats are made.

File grievances via the RBI Complaint Management System.

For personalized help, visit ExpertPanel.org — our financial experts and legal advisors can guide you through loan restructuring or harassment issues.

Smart Rule Before You Swipe

Buying on EMI isn’t always wrong — but it demands discipline. Before every purchase, ask: “Do I need this now, or am I just delaying financial pain?” EMI par phone lena easy hai… Par 24 mahine tak recovery waalon se bachna impossible! Socho, samjho, aur phir swipe karo.

Conclusion

EMI is not “Easy Monthly Installment” — it’s Every Month’s Impact on your future. A smart borrower doesn’t just buy today — they think about tomorrow’s peace of mind. Stay informed. Stay debt-free. For expert consultation on loan management or restructuring, visit ExpertPanel.org today.